The $280 Billion AI Arms Race: How Tech Giants Are Leveraging Bond Markets to Build the Future

An in-depth analysis of capital expenditure and debt financing strategies in the age of artificial intelligence — written purely out of curiosity.

INTRODUCTION

In the decade spanning 2015 to 2025, the world's largest technology companies embarked on what may be the most significant infrastructure buildout in corporate history. Driven by the explosive rise of artificial intelligence and the race to dominate the next computing paradigm, these firms have collectively increased their capital expenditures from $77 billion to over $280 billion annually—a staggering 264% increase that dwarfs even the mobile and cloud computing transitions of the previous decade.

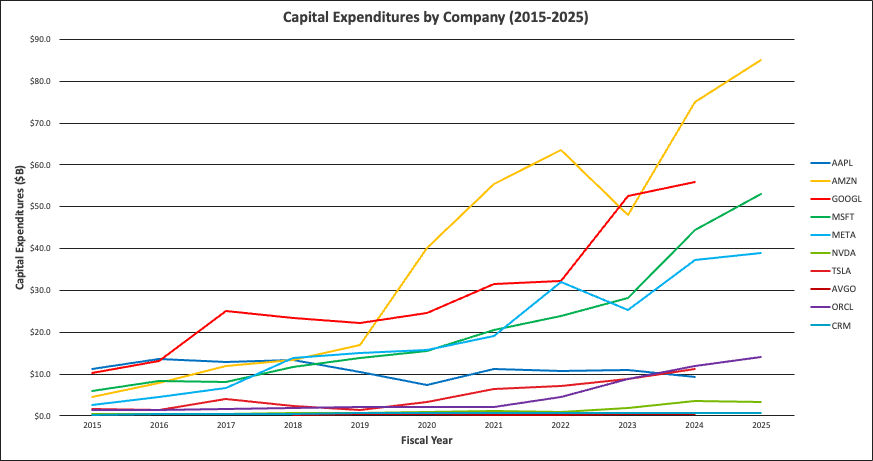

But this unprecedented investment spree didn't happen in isolation. Behind the scenes, these companies have strategically leveraged global bond markets, issuing over $400 billion in long-term debt to finance data centers, specialized AI chips, and computing infrastructure at a scale previously unimaginable. The story of how Apple, Microsoft, Alphabet, Amazon, Meta, NVIDIA, Tesla, Broadcom, Oracle, and Salesforce are funding the AI revolution offers critical insights into corporate finance, technology strategy, and the future of the digital economy.

THE CHATGPT MOMENT: WHEN AI BECAME REAL

November 2022 marked an inflection point. When OpenAI released ChatGPT to the public, it wasn't just a product launch—it was a starting gun for the most intense capital deployment race in technology history. Within months, every major tech company announced massive increases in artificial intelligence investments, triggering a capital expenditure acceleration that continues to reshape corporate balance sheets.

The numbers tell the story:

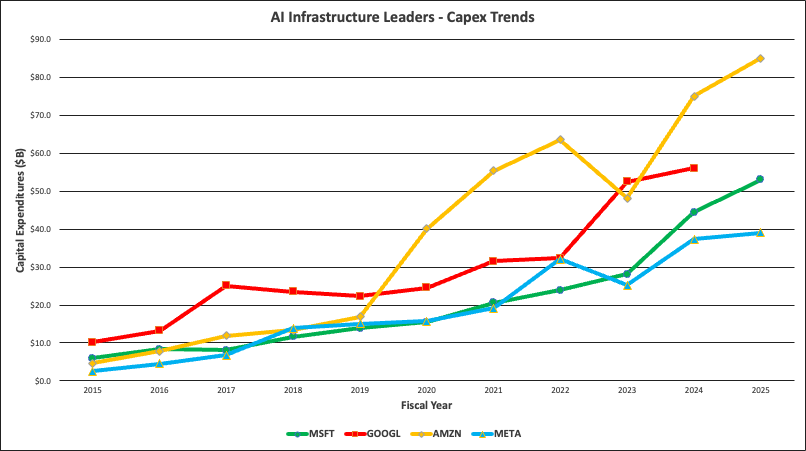

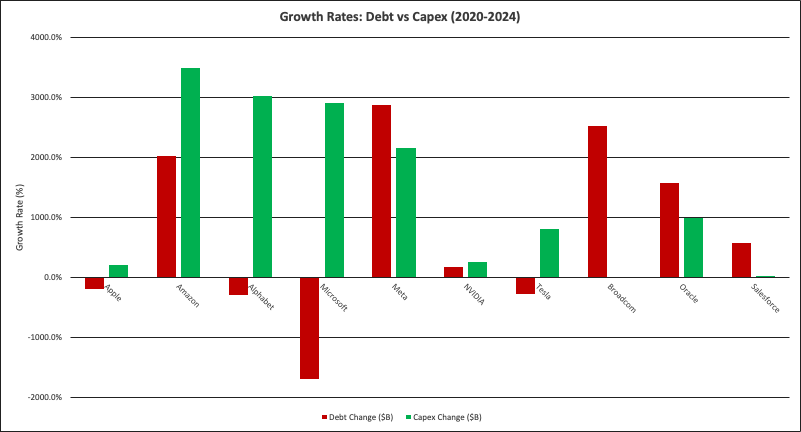

These aren't just incremental increases—they represent a fundamental reallocation of corporate resources toward AI infrastructure. Microsoft alone went from spending $15.4 billion on capital expenditures in 2020 to a projected $53 billion in 2025, a 244% increase in just five years. Alphabet's trajectory is even more dramatic: from $22.3 billion to $56 billion over the same period, a 151% increase.

THE BIG FOUR: WHO'S LEADING THE CHARGE

Four companies have emerged as the undisputed leaders in AI infrastructure spending: Microsoft, Alphabet, Amazon, and Meta. Together, they account for approximately $188 billion in annual capital expenditures—roughly 67% of the total spending across all ten companies analyzed. Their investments focus on three critical areas:

- Data Center Expansion

Building and equipping massive facilities to house AI training clusters. These aren't traditional data centers—they require specialized cooling systems, power infrastructure capable of handling megawatt-scale GPU clusters, and networking equipment that can handle the unprecedented bandwidth requirements of large language model training.

- Custom Silicon Development

Companies like Alphabet (with its TPU chips) and Amazon (with Trainium and Inferentia) are investing billions in developing proprietary AI processors to reduce dependence on NVIDIA and gain competitive advantages in model training efficiency.

- Global Network Infrastructure

Connecting data centers, building edge computing locations, and creating the high-speed networks necessary to deliver AI services globally with low latency.

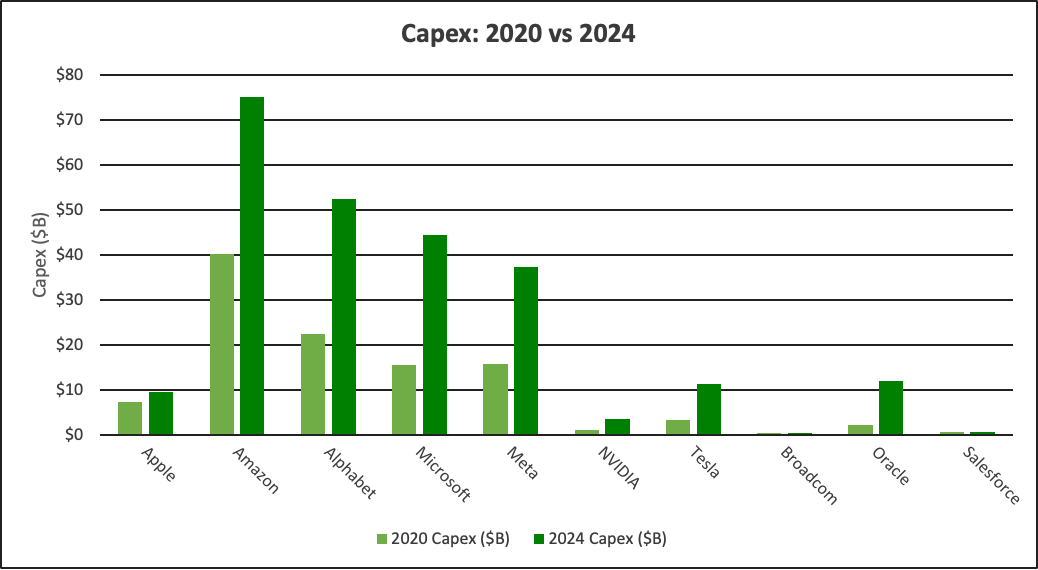

EXPLOSIVE GROWTH: 2020 VS 2024 COMPARISON

FINANCING THE FUTURE: THREE DEBT STRATEGIES

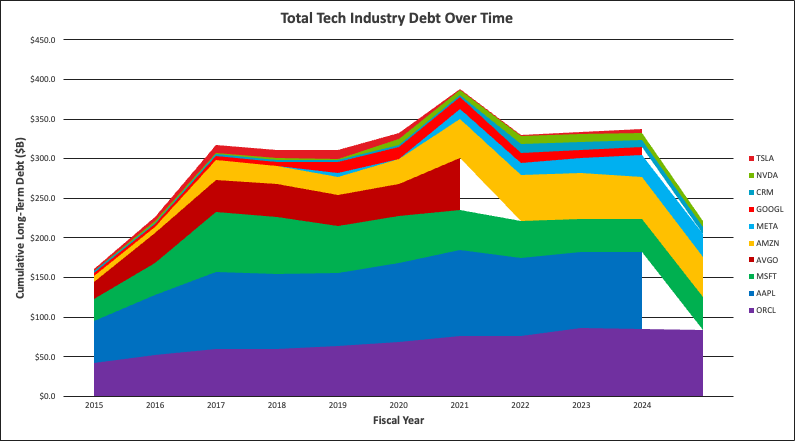

While the scale of capital expenditure is unprecedented, equally fascinating is how these companies are financing it. With total long-term debt exceeding $400 billion across the ten companies, three distinct approaches have emerged:

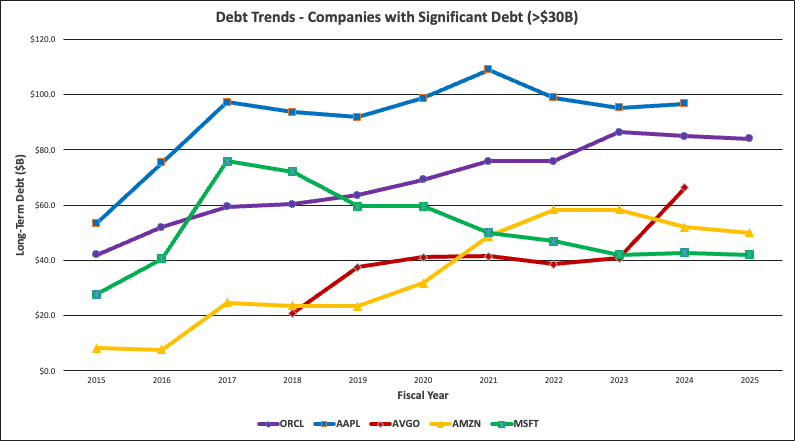

Strategy 1: The High Leverage Approach (Oracle, Broadcom, Apple)

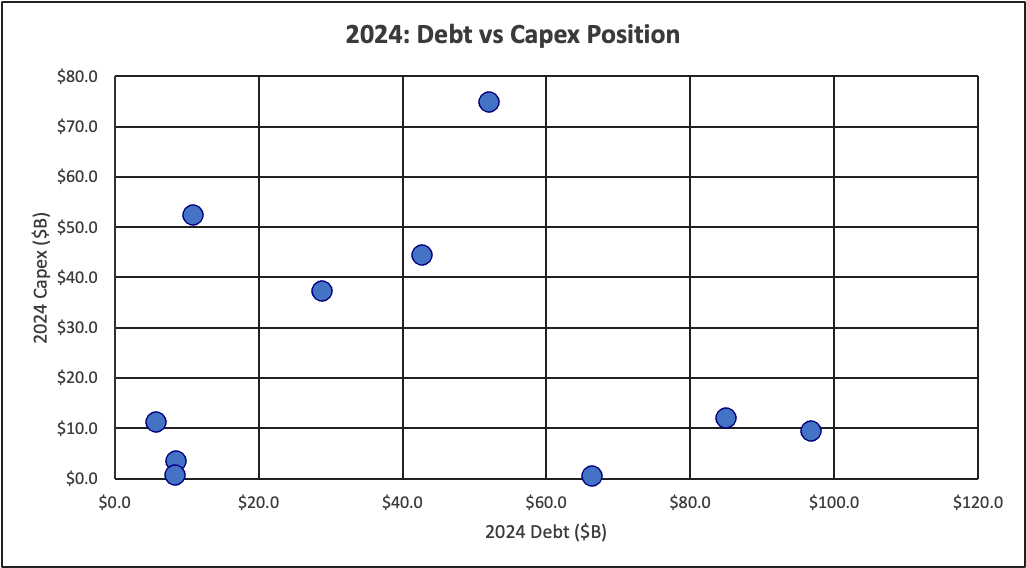

Oracle leads this category with $85 billion in long-term debt and a debt-to-Capex ratio of 7.08x—the highest among all companies analyzed. This aggressive leverage strategy reflects Oracle's push into cloud infrastructure (Oracle Cloud Infrastructure Gen2) and its need to compete with established players like AWS and Azure. The company has consistently used debt markets to fund both infrastructure buildout and strategic acquisitions.

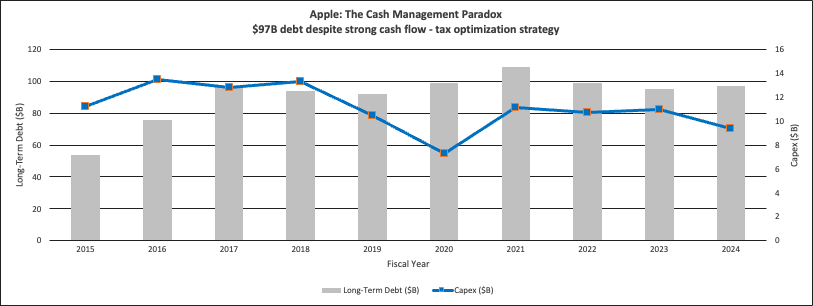

Apple, despite generating massive free cash flow, maintains approximately $97 billion in debt. However, this reflects a deliberate capital allocation strategy: borrowing at low rates to fund share buybacks and dividends while keeping overseas cash untaxed. Apple's debt-to-Capex ratio of 10.3x is misleading—the company isn't borrowing to fund operations but rather to optimize its capital structure.

Broadcom's debt increased dramatically from $41 billion to $66 billion in 2024, largely due to acquisition financing (notably the VMware acquisition). Unlike other companies, Broadcom's Capex remains minimal ($0.5B annually), reflecting a business model focused on acquisitions rather than organic infrastructure investment.

Strategy 2: The Balanced Approach (Amazon, Microsoft)

Amazon and Microsoft represent a middle path. Amazon maintains approximately $52 billion in debt while spending $75 billion annually on capital expenditures—a debt-to-Capex ratio of 0.69x. This balanced approach allows Amazon Web Services to expand aggressively while maintaining financial flexibility. The company has actually been reducing leverage (debt declined from $58.3B in 2022) even as Capex accelerated.

Microsoft's story is even more striking. The company has reduced its long-term debt from $76 billion in 2017 to approximately $42 billion in 2024, even while tripling capital expenditures from $15.4 billion to $44.5 billion. This represents a deliberate deleveraging strategy, using strong operating cash flows to fund growth while reducing financial risk. Microsoft's debt-to-Capex ratio of 0.96x reflects this conservative approach.

Strategy 3: The Cash-Rich Conservative Approach (Alphabet, NVIDIA, Meta)

Alphabet exemplifies this strategy with only $11 billion in debt against $52.5 billion in annual Capex—a debt-to-Capex ratio of just 0.21x, the lowest in the group. The company relies almost entirely on its massive operating cash flows (over $80 billion annually) to fund infrastructure investments. This conservative approach provides maximum financial flexibility and reflects management's confidence in sustained cash generation.

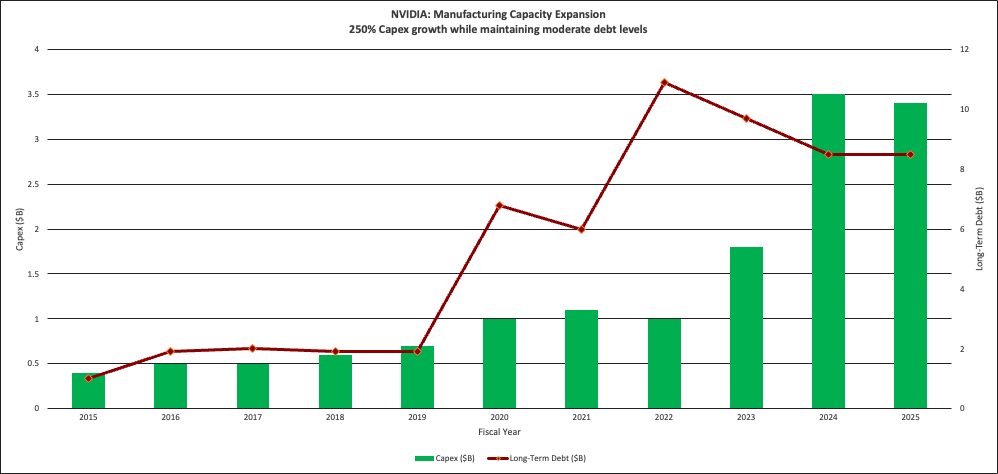

NVIDIA's debt position ($8.5 billion) is modest relative to its market capitalization, though its debt-to-Capex ratio (2.43x) is higher than Alphabet's. The company has increased debt strategically to fund manufacturing capacity expansion for H100 and H200 GPU production—critical infrastructure for the AI boom it's enabling.

Meta presents an interesting case. The company went from essentially zero debt in 2020 to $29 billion in 2024, using bond markets strategically to fund its massive investments in Llama AI models and Reality Labs (the metaverse division). Despite this increase, Meta's debt-to-Capex ratio remains conservative at 0.77x.

THE MECHANICS: HOW TECH COMPANIES USE BOND MARKETS

The bond issuance strategies employed by these companies reveal sophisticated approaches to capital markets:

Fixed-Rate Corporate Bonds: The Primary Tool

Companies like Apple, Microsoft, and Oracle primarily issue fixed-rate senior unsecured notes with maturities ranging from 5 to 30 years. This approach serves several strategic purposes:

- Lock in low interest rates: During the 2020-2021 period, companies issued debt at historically low rates (often below 3%), creating a permanent capital cost advantage

- Match asset lifespans: Data centers have useful lives of 15-20 years, making long-term debt an appropriate financing match

- Maintain investment grade ratings: All ten companies maintain strong credit ratings (AA to BBB+), enabling access to capital markets at favorable terms

- Create predictable cost structures: Fixed rates eliminate interest rate risk and create budget certainty

Commercial Paper and Short-Term Flexibility

Companies like Microsoft and NVIDIA supplement long-term bonds with commercial paper programs—short-term debt instruments that provide working capital flexibility. These programs typically run 30-270 days and offer lower rates than long-term bonds, though they require continuous refinancing.

Private Credit: The Supplementary Source

While public bond markets dominate, companies increasingly use private credit arrangements for specific projects or to maintain relationships with key financial institutions. Private credit offers:

- Speed: Faster execution than public offerings

- Flexibility: Customized terms for specific needs

- Privacy: No public disclosure requirements

- Relationship banking: Maintains credit lines and banking relationships

However, private credit typically commands higher interest rates than public bonds and is used selectively rather than as a primary financing source.

THE ORACLE EXCEPTION: AGGRESSIVE GROWTH THROUGH DEBT

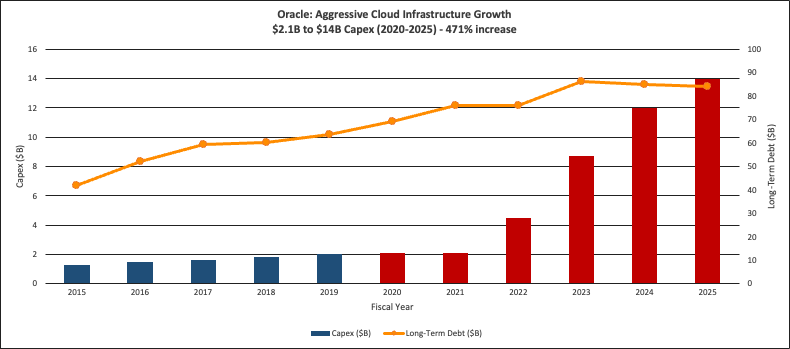

Oracle deserves special attention as the most dramatic growth story in the dataset. From $2.1 billion in Capex in 2020 to $12 billion in 2024—a staggering 471% increase—Oracle is making an all-out push to establish Oracle Cloud Infrastructure (OCI) as a viable alternative to AWS, Azure, and Google Cloud.

What makes Oracle's approach particularly noteworthy is its willingness to leverage the balance sheet aggressively. With $85 billion in debt (the second-highest absolute level after Apple), Oracle is essentially betting the company on winning a share of the cloud computing market. The strategy focuses on:

- AI-optimized infrastructure: OCI Gen2 data centers designed specifically for AI workloads

- Competitive pricing: Using scale to offer lower prices than established competitors

- Enterprise partnerships: Leveraging existing database customer relationships to cross-sell cloud services

- Government and healthcare: Targeting regulated industries with compliance-focused offerings

The question facing Oracle is whether this massive debt-funded investment will generate returns sufficient to justify the financial risk. The company is essentially racing against time to capture market share before its debt service becomes unsustainable.

NVIDIA'S UNIQUE CHALLENGE: MANUFACTURING CONSTRAINTS

NVIDIA occupies a unique position in this landscape. Unlike the other companies building data centers to consume AI compute, NVIDIA must manufacture the specialized GPUs that power AI training and inference. This creates a different capital expenditure profile:

The company's Capex increased from $1.0 billion in 2020 to $3.5 billion in 2024—a 250% increase that, while impressive in percentage terms, remains far smaller in absolute dollars than the infrastructure companies. This reflects NVIDIA's asset-light manufacturing model: the company designs chips but outsources production to TSMC and other foundries.

However, NVIDIA faces increasing pressure to secure manufacturing capacity. With demand for H100 and H200 GPUs vastly outstripping supply, the company must:

- Invest in advanced packaging facilities (critical for chiplet-based designs)

- Build design and validation centers

- Expand testing and quality assurance infrastructure

- Develop next-generation chip designs

NVIDIA's $8.5 billion debt position reflects this balancing act: enough leverage to expand capacity quickly, but not so much as to risk the company's financial flexibility if the AI boom moderates.

THE OUTLIERS: APPLE AND TESLA'S DIFFERENT PATHS

Apple: The Cash Management Paradox

Apple presents a fascinating paradox. Despite generating approximately $100 billion in annual free cash flow, the company maintains $97 billion in debt—the highest absolute level in the group. But Apple's debt isn't funding growth; it's optimizing capital structure.

The strategy is straightforward: Apple holds significant cash overseas (from international iPhone and services revenue). Rather than repatriating that cash and paying U.S. taxes, the company borrows domestically at low rates to fund:

- Share buybacks: Over $90 billion annually in recent years

- Dividends: Approximately $15 billion in annual payments

- Modest operational investments: $9-11 billion in annual Capex

This arbitrage generates value: borrowing at 3% costs less than the 21% corporate tax rate on repatriated foreign earnings. Apple's Capex has actually declined slightly from its peak, reflecting the company's shift toward services and away from hardware manufacturing infrastructure.

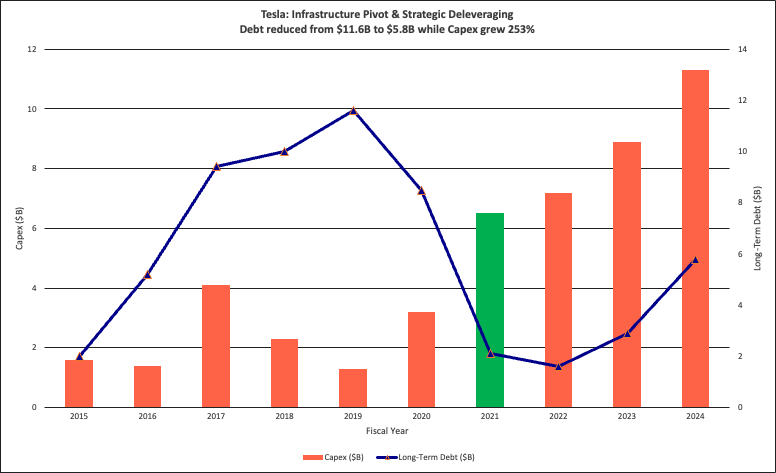

Tesla: The Infrastructure Pivot

Tesla's capital expenditure story reflects its evolution from automotive startup to diversified technology company. Capex increased from $3.2 billion in 2020 to $11.3 billion in 2024—a 253% increase driven by:

- Gigafactory expansion: New facilities in Texas, Germany, and planned locations

- 4680 battery cell production: Vertical integration into battery manufacturing

- Full Self-Driving infrastructure: The Dojo supercomputer for neural network training

- Charging network: Expanding Supercharger infrastructure

- Optimus robot development: Manufacturing capabilities for humanoid robots

Interestingly, Tesla has dramatically reduced its debt from $11.6 billion in 2019 to just $5.8 billion in 2024. The company has shifted from debt-dependent to cash-flow-funded, reflecting improved profitability and strong free cash flow generation. This deleveraging while simultaneously increasing Capex demonstrates Tesla's improving financial position.

INDUSTRY IMPLICATIONS: WHAT THIS MEANS FOR TECHNOLOGY

The Concentration of Computing Power

One of the most significant implications of this capital deployment is the increasing concentration of AI computing power among a handful of companies. When four firms (Microsoft, Alphabet, Amazon, Meta) account for $188 billion in annual infrastructure spending, they effectively create insurmountable moats:

- Scale advantages: Larger deployments mean lower per-unit costs for computing, power, and networking

- Talent attraction: The best AI researchers want access to the largest computing clusters

- Data advantages: More infrastructure enables processing larger datasets, creating better models

- Network effects: Once customers build on a platform, switching costs become prohibitive

This creates a winner-takes-most dynamic where smaller competitors struggle to match the scale and capability advantages of infrastructure leaders.

The Power and Sustainability Challenge

Data centers now consume approximately 1-2% of global electricity, and AI workloads are dramatically more power-intensive than traditional computing. A single large language model training run can consume megawatts of power for weeks or months. This creates multiple challenges:

- Grid capacity: Many regions lack electrical infrastructure to support megawatt-scale data centers

- Renewable energy: Tech companies have committed to carbon neutrality, requiring massive renewable energy investments

- Cooling systems: AI chips generate extreme heat, requiring advanced cooling technologies

- Location constraints: Data centers must locate near power sources, affecting geographic distribution

Companies are responding by investing in on-site power generation (including exploring small modular nuclear reactors), advanced cooling technologies, and more efficient chip designs. These infrastructure costs are embedded in the Capex figures but represent an increasing share of total spending.

The Geopolitical Dimension

The concentration of AI infrastructure has geopolitical implications. The United States hosts the majority of this computing capacity, creating both economic advantage and strategic concerns:

- Export controls: U.S. restrictions on advanced chip exports to China affect NVIDIA and limit competitors' access

- Data sovereignty: Countries increasingly demand local data storage, driving regional data center buildouts

- Technology competition: China's efforts to build independent AI infrastructure create parallel ecosystems

- National security: AI capabilities are increasingly viewed through security and defense lenses

These dynamics will shape future investment patterns and may lead to more geographically distributed infrastructure than current trends suggest.

RISKS AND UNCERTAINTIES: WHAT COULD GO WRONG

The Utilization Question

The single biggest risk facing these companies is whether AI infrastructure will generate returns commensurate with investment. Several scenarios could undermine the current buildout:

- Slower AI adoption: If enterprises adopt AI more slowly than expected, data center utilization could disappoint

- Model efficiency gains: Better algorithms could reduce compute requirements, making existing infrastructure over-capacity

- Competitive pricing pressure: Excess capacity could trigger price wars, compressing margins

- Technology shifts: New approaches (e.g., smaller, more efficient models) could disrupt current architecture assumptions

Microsoft, Alphabet, and Amazon partially mitigate this risk through cloud services—they can rent unused capacity to other companies. But Meta, Tesla, and others building dedicated AI infrastructure face higher utilization risk.

Debt Service in a Rising Rate Environment

While most debt was issued at favorable rates (2020-2021), refinancing requirements create interest rate risk. Companies with high leverage face particular challenges:

- Oracle: $85B debt at higher rates could significantly increase interest expense

- Broadcom: Recent debt issuance for VMware acquisition carries higher costs

- Refinancing risk: Bonds issued at 2-3% must eventually be refinanced at 5-6% or higher

Lower-leverage companies (Alphabet, Meta) face minimal refinancing risk, while high-leverage players must manage this carefully.

Regulatory and Antitrust Concerns

The concentration of AI computing power is attracting regulatory scrutiny:

- Antitrust investigations: European and U.S. regulators are examining AI market power

- Data privacy: GDPR and similar regulations affect data center operations

While unlikely to stop infrastructure buildouts, regulation could slow deployment or increase costs.

Technical Obsolescence

The AI field evolves rapidly. Infrastructure built for today's large language models may not suit tomorrow's approaches:

- Quantum computing: Could disrupt classical computing infrastructure

- Neuromorphic chips: Brain-inspired architectures might require different infrastructure

Data center depreciation schedules (15-20 years) assume technology remains relevant—a significant assumption.

LOOKING AHEAD: THE NEXT FIVE YEARS

Sustained High Investment Levels

All indicators suggest capital expenditure will remain elevated through at least 2027-2028:

- Company guidance: Microsoft, Alphabet, and Amazon have signaled continued high Capex

- Competitive dynamics: No company can afford to fall behind in AI infrastructure

- Workload growth: AI inference (running models) is growing faster than training, requiring more infrastructure

- New use cases: AI agents, video generation, and scientific computing will drive additional demand

Expect total industry Capex to reach $350-400 billion annually by 2027, representing 40-50% growth from current levels.

Debt Market Dynamics

The corporate bond market will continue to play a crucial role:

- Refinancing wave: $100B+ in tech debt matures 2025-2027, requiring refinancing at higher rates

- New issuance: Companies will issue $50-75B in new bonds annually to fund infrastructure

- Credit quality: Strong cash flows should maintain investment grade ratings despite higher leverage

- Private credit growth: Expect increased use of private credit for flexible, project-specific financing

Consolidation and Shakeout

Not all companies will succeed in justifying their investments:

- Oracle's moment of truth: The company's aggressive strategy will be tested as OCI either gains traction or struggles to compete

- Specialized players: Companies like Salesforce may need to partner rather than build infrastructure

- Acquisition targets: Smaller cloud players could become attractive acquisition targets for infrastructure leaders

- Market consolidation: The 'Big Three' cloud providers (AWS, Azure, Google Cloud) may increase market share dominance

Efficiency and Optimization Phase

After the current buildout frenzy, expect a shift toward optimization:

- Model efficiency: Dramatic improvements in model architecture will reduce compute requirements

- Chip specialization: Custom silicon from Alphabet, Amazon, and others will improve performance per dollar

- Workload optimization: Better scheduling and resource management will increase utilization

- Cost discipline: Shareholders will demand ROI visibility, forcing more careful investment

This could lead to Capex moderation by 2028-2029, though absolute levels will remain far above pre-2022 baselines.

CONCLUSION: THE INFRASTRUCTURE THAT DEFINES A GENERATION

The $280 billion AI infrastructure buildout represents more than just corporate capital allocation—it's the foundation for a technological transition as significant as the move from mainframes to personal computers, or from desktop software to cloud services.

The companies leading this charge—Microsoft, Alphabet, Amazon, and Meta—are making decade-defining bets that AI will transform virtually every industry and use case. Their willingness to deploy over $400 billion in debt to accelerate this buildout demonstrates conviction that the AI revolution is real, substantial, and here to stay.

Three key insights emerge from this analysis:

- Scale Creates Moats

The companies investing most aggressively are creating sustainable competitive advantages through sheer scale. When Alphabet spends $52.5 billion on Capex annually, it's not just buying data centers—it's building moats that smaller competitors cannot cross. This concentration of AI computing power will shape the industry for decades.

- Debt Is Strategic, Not Desperate

"These aren't companies borrowing because they must—they're borrowing because it's strategically advantageous. Lock in low rates, match long-lived assets with long-term financing, preserve cash for flexibility, and accelerate deployments. The divergent approaches (Oracle's aggression vs. Alphabet's conservatism) show there's no single ""right"" answer, but all are deliberate choices."

- The Winner-Takes-Most Dynamic Is Intensifying

As infrastructure requirements grow, the advantages of scale compound. Companies that can deploy $50+ billion annually can negotiate better terms with suppliers, attract top talent, process larger datasets, and iterate faster. This creates a self-reinforcing cycle where leaders extend their leads.

For investors, policymakers, and industry observers, the implications are profound. The AI revolution won't be democratized—it will be concentrated among companies with the capital, expertise, and willingness to make enormous long-term bets. The bond markets enabling this transformation are just as important as the technology itself.

Whether these investments generate appropriate returns remains to be seen. But one thing is certain: the companies making these bets are reshaping not just technology, but the global economy itself. The data centers being built today will process the AI workloads defining the 2030s and beyond.

The $280 billion question is whether this infrastructure will power the next industrial revolution—or become the most expensive overcapacity ever built. The answer will determine the winners and losers of the AI era.

Data Sources: SEC 10-K and 10-Q filings (2015-2025)

Companies Analyzed: Apple (AAPL), Microsoft (MSFT), Alphabet (GOOGL), Amazon (AMZN), Meta (META), NVIDIA (NVDA), Tesla (TSLA), Broadcom (AVGO), Oracle (ORCL), Salesforce (CRM)